India is reeling from a power crisis, which no one saw coming even as recently as two weeks ago. A mix of various factors including jump in demand following post-COVID economic recovery, depressed renewable power output, fall in domestic coal production and spike in international coal prices has squeezed coal supply and, in turn, led to power shortages and blackouts in multiple states.

Moving 12-month power demand growth, after falling to a low of -7.5% in August 2020, has slowly crept up and increased to over 10% by September 2021. However, growth in renewable power output including power from hydro and biomass sources has hovered around 3-4% in the last year partly because of exceptionally low wind speeds.

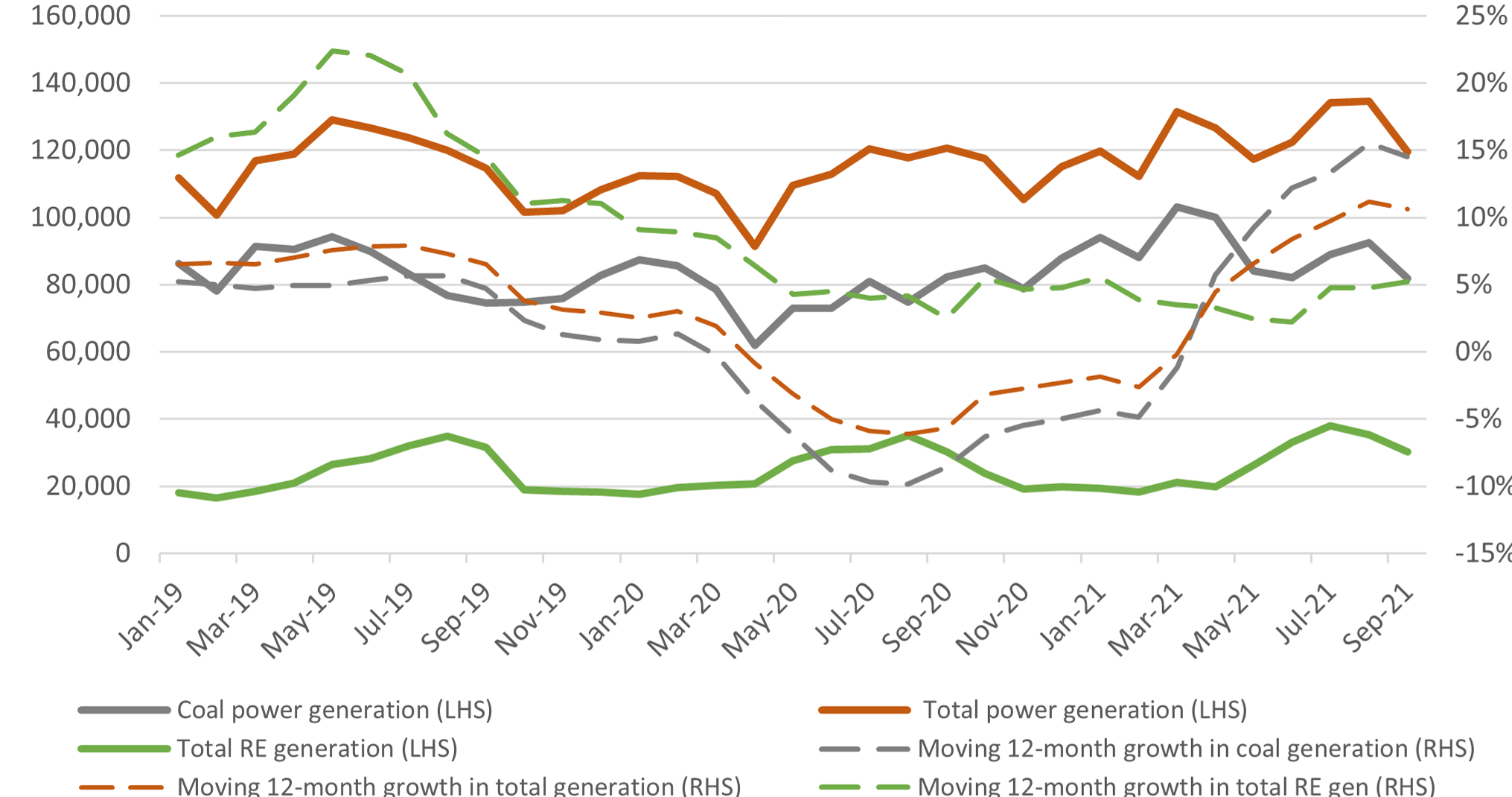

Figure 1: Coal and total power generation in India, million kWh

Source: CEA, POSOCO, BRIDGE TO INDIA research

Note: RE generation includes power from all renewable sources including solar, wind, large hydro, small hydro and biomass.

As the only effective balancing source available, coal shoulders heavy burden of meeting residual demand. As Figure 1 shows, coal power output has grown faster (15% in the last 12 months) than total power generation (10.6%). This has eaten into coal stocks as domestic production has failed to keep up (hit by flooding of some mines) and imports have fallen (spike in international prices). Average coal inventory at power plants has fallen from 15 days one year ago to just 3 days or less at many plants.

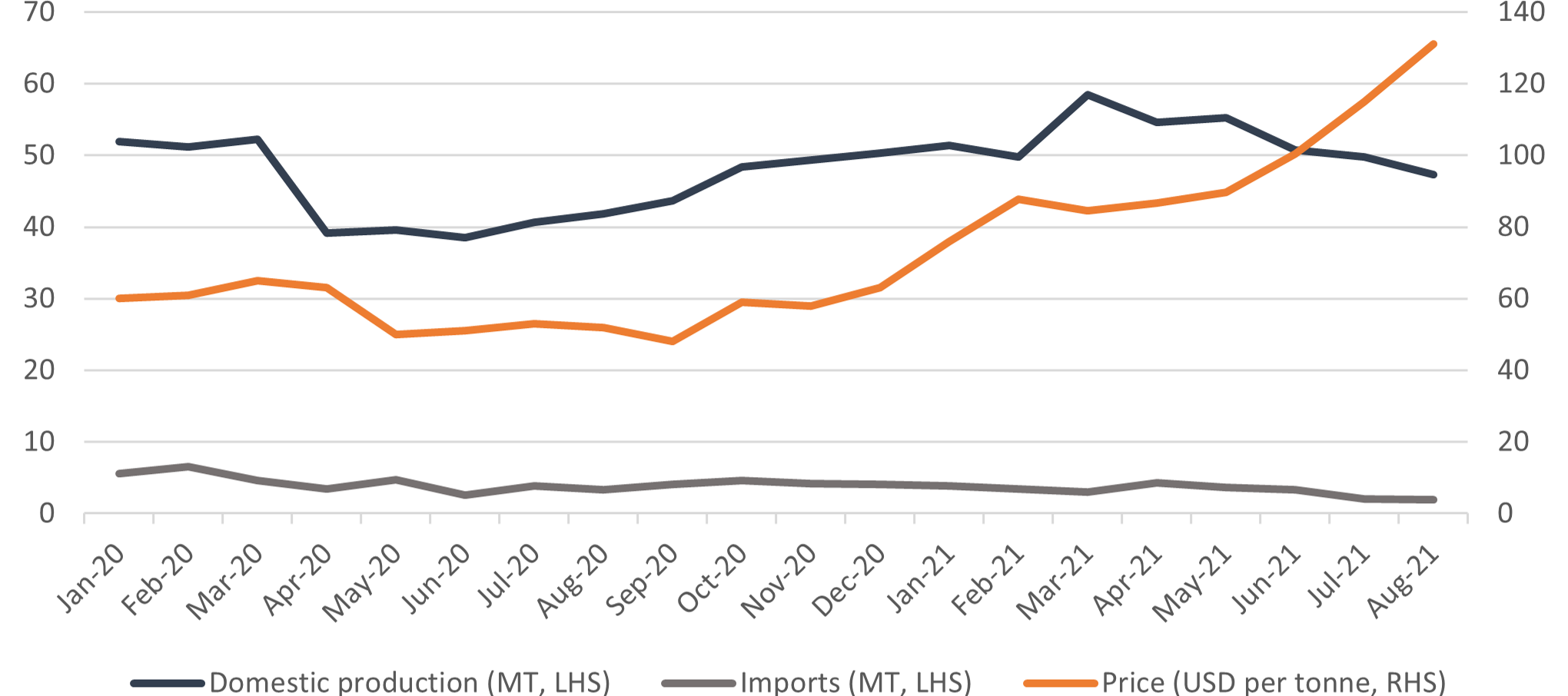

The government is now proposing higher coal imports despite trebling of international coal prices since September 2020. This is clearly an unworkable plan as DISCOMs/ consumers are not willing to bear higher prices and international freight channels are severely congested. As Figure 2 shows, imports have now shrunk month-on-month for the last five months.

Figure 2: Domestic coal production, imports and international prices

Source: CEA

Coal India, the PSU giant, is dealing with its own precarious problems ranging from diminution of financing and management capacity to delayed payments by power producers. Attempts to make India self-sufficient in coal have borne little results with stagnant production trailing behind targets by huge margins.

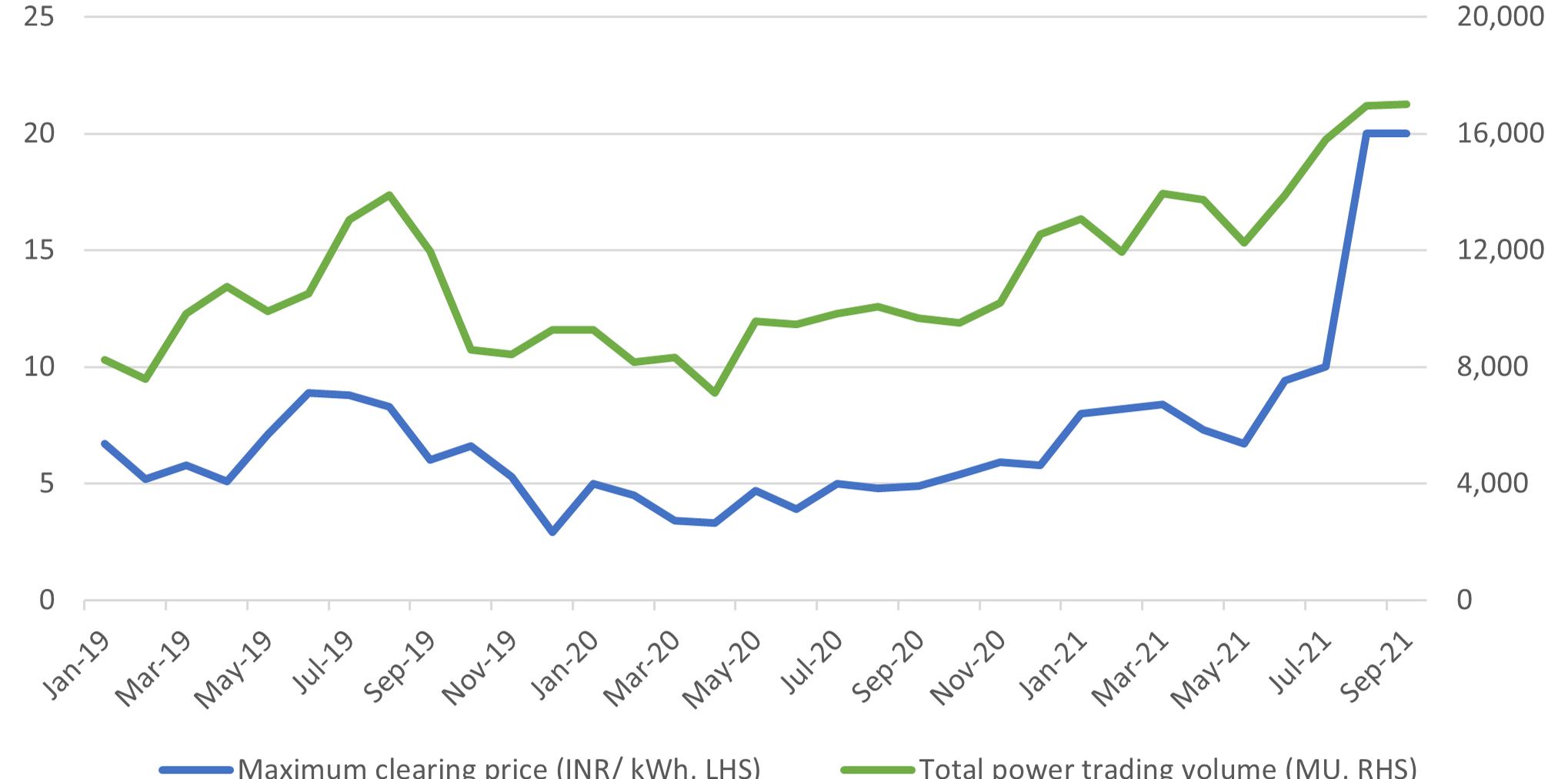

Amidst a deteriorating demand-supply balance, short-term trading volume and prices have soared as seen in Figure 3. Peak hour tariffs in the real-term market platform have repeatedly breached INR 20.00/ kWh mark in the past month.

Figure 3: Short-term power trading volume and peak tariffs at Indian Energy Exchange

Sources: IEX, NLDC, CERC

Note: Short-term trading volume includes power traded on exchanges and in the bilateral market.

Events of these last two weeks show just how critically the entire power sector is stretched to a breaking point. It is important to draw right lessons from this crisis, surely one of many more to come, as share of intermittent renewable power with must-run status increases. The entire value chain needs more resilience and reform with strengthening of institutional capacity, more reliable payment streams and market-oriented trading mechanisms besides robust long-term planning.