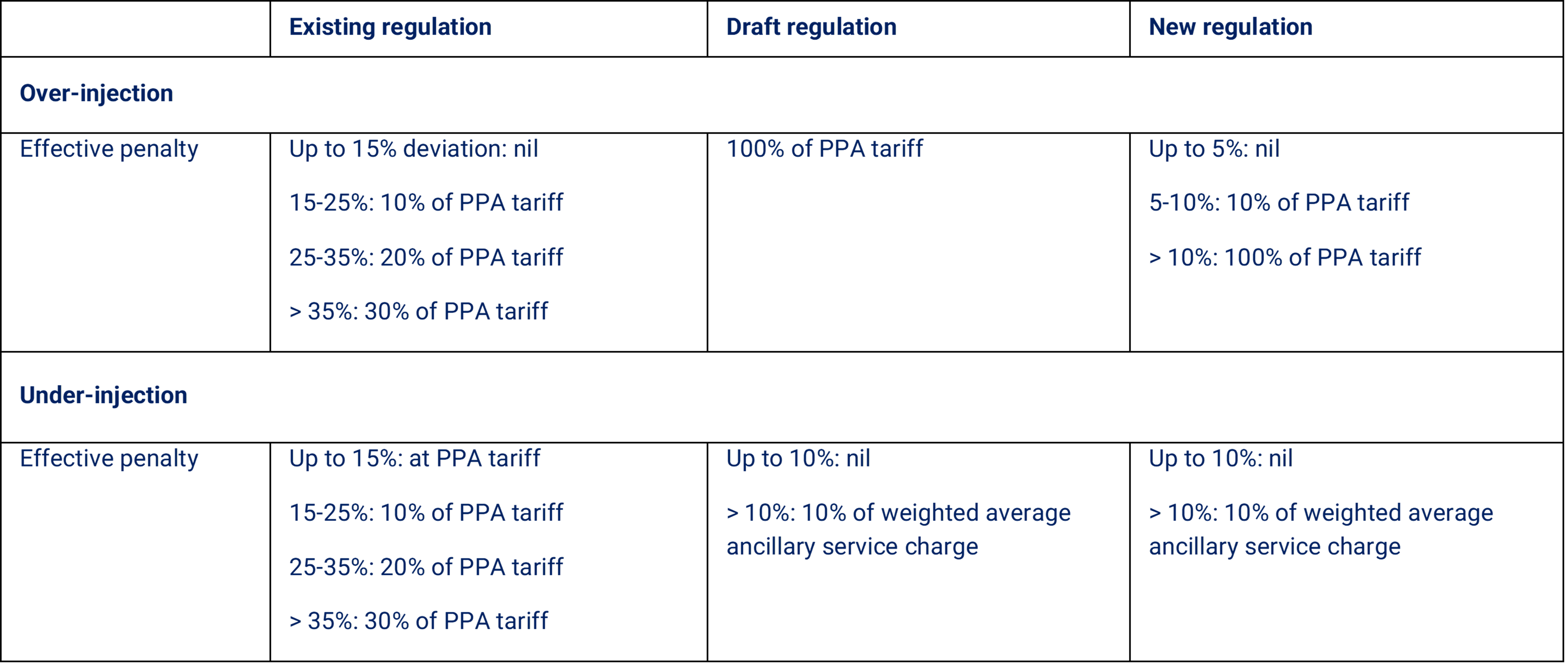

CERC, India’s central power sector regulator, has revised regulations pertaining to the Deviation Settlement Mechanism (DSM) for solar and wind power projects. The regulator has both tightened the deviation bands and increased penalties for deviations. Consequences for over-injection are considerably worse with developers not to be paid anything for more than 10% extra output. Penalty for under-injection has been restructured and linked to ancillary service charges for secondary and tertiary services instead of PPA tariff.

CERC has justified making the regulation more stringent by claiming improvement in forecasting accuracy and low penalties for individual power producers due to aggregation of schedules at pooling station. Effective date of the new regulation is yet to be notified.

Table: Deviation bands and penalties under previous and revised regulations

Notes: 1. In practice, penalties are imposed on power producers on top of their entitlement for power sale payments on the basis of power scheduled quantum. Effective penalty figures in this table are presented on a net basis after accounting for payment due for scheduled power. 2. In FY 2022, weighted average ancillary service charge was INR 6.91/ kWh.

It is worth recalling that all renewable projects are required to forecast and schedule their power output in 15-minute intervals on a day-ahead basis. They may revise the schedule up to 16 times a day subject to one revision for each time slot of 1.5 hours. The objective of these regulations, which apply to all renewable power projects, DISCOMs and consumers connected to the national grid, is to minimise scheduling deviations in order to maintain grid stability and security.

Following the new CERC regulation, the states are expected to revise their respective regulations. Most state regulations follow deviation bands defined by CERC and levy penalties of INR 0.50-1.50/ kWh depending on the amount of deviation. However, some states including Gujarat, Haryana, Madhya Pradesh and Tamil Nadu have defined tighter bands. Gujarat has adopted the tightest bands at 7% for solar power and 8-12% for wind power. Andhra Pradesh even tried to remove deviation bands altogether with a proposed flat penalty of INR 2.00/ kWh for all deviations exceeding 4.89%. But following strong opposition from the developers, the state regulator withdrew draft regulation and introduced 10% tolerance bands.

The new regulation is considerably more penal for over-injection and hence, inadvertently promotes over-scheduling. An analysis of a 250 MW solar power project in Rajasthan shows a sharp increase in penalty impact under new DSM bands. Average annual penalty amount is expected to increase from about 0.15% of revenues to 1.65% of revenues for the same schedule. However, a shift to over-scheduling can bring down annual penalty amount to about 0.5-0.8% of revenues. This amount should come down further over time as the industry adapts to new regulations and forecasting ability improves.

Another unintended consequence of the new regulation and deliberate over-scheduling by renewable IPPs would be increase in real-time and ancillary services trading volumes since actual renewable power output is likely to be lower than the scheduled amount.

This report provides a quarterly update on key trends and developments in the corporate renewable market including capacity addition, key players, pol...

This report provides a detailed update of all key sector developments and trends in the quarter – capacity addition, leading players, tenders and po...

India’s corporate renewable market is becoming more vibrant with strong demand, policy and technology levers. Driven by net zero targets and investo...

Green hydrogen is a versatile fuel which may be used as an energy store, fuel and feedstock across multiple sectors. Refining and fertiliser industrie...

A business case for renewable energy certificates for Indian companies to meet RE 100 targets

C&I consumers account for 53% of power consumption but only 6% of this requirement is met from direct procurement of renewable power. In face of m

Price :

Apply now

Register

Arrange Trial Session

Developing a corporate renewable procurement roadmap

Register Now

Advanced clean energy technologies

Register Now

We use cookies to offer you an optimal user experience and collect information on website usage.

Login

Or

Sign up

Sign up to our free monthly bulletin, blogs and reports

Terms and conditions

Introduction

These terms and conditions govern your use of our website – bridgetoindia.com. By using our website, you accept these terms and conditions in full; if you disagree with any part of these terms and conditions, you must not use our website.

You must be at least 18 years of age to use our website; by using our website, you warrant and represent to us that you are at least 18 years of age.

Our details

This website is owned and operated by BRIDGE TO INDIA Energy Private Limited.

We are registered in India under registration number CIN: U40106 HR2008 PTC058267, and our registered office is at C8/5 DLF 1, Gurugram 122001, INDIA.

Our principal place of business is at C8/5 DLF 1, Gurugram 122001, INDIA.

Our GST number is 06AADCB 6783 D1ZQ.

You can contact us by post at the address given above or by telephone on +91-124-420-4003 or by email at contact@bridgetoindia.com

Ownership and licence to use

All information and content on our website is owned exclusively by us. We reserve the right to discontinue or alter any or all of the website content at any time.

The website contents are protected by Indian copyright and international copyright/intellectual property laws under applicable treaties and/or conventions.

We grant you a personal, non-exclusive, non-transferable licence to use the website.

We reserve the right to restrict access to our website at our discretion; you must not circumvent or bypass, or attempt to circumvent or bypass, any such access restriction measures.

Acceptable use

You must not edit or modify any material on our website.

You must not:

sell, rent or sub-license material from our website;

share, reproduce or copy any material from our website without our express written consent.

You must not:

use our website in any way or take any action that causes, or may cause, damage to the website or impairment of the performance, availability or accessibility of the website;

use our website in any way that is unlawful, illegal, fraudulent or harmful;

conduct any systematic or automated data collection activities (including without limitation scraping, data mining, data extraction and data harvesting) on or in relation to our website;

use data collected from our website for any direct marketing activity (including without limitation email marketing, SMS marketing, telemarketing and direct mailing).

Limited warranties

We do not warrant or represent completeness or accuracy of the information published on our website. The information available on our website is of general use and may not be suitable for you.

We aim to provide accurate and up-to-date information but are not legally liable for the accuracy of such information.

You use our website at your own risk.

To the maximum extent permitted by applicable law, we exclude all representations and warranties relating to the subject matter of these terms and conditions, our website and the use of our website.

Registration and accounts

You may register for an account with our website by completing and submitting the account registration form on our website.

You must keep your password confidential.

You must not use any other person's account to access the website.

You must not allow any other person to use your account to access the website.

You must notify us in writing immediately if you become aware of any unauthorised use of your account.

We may suspend or cancel your account at any time in our sole discretion without notice or explanation.

Purchases

All purchases made on this website are non-refundable and non-exchangeable.

Your content

In these terms and conditions, "your content" means all information and materials (including without limitation text, graphics, images, audio material, video material, audio-visual material, scripts, software and files) that you submit to us for storage or publication on, processing by, or transmission via, our website.

You grant to us a worldwide, irrevocable, non-exclusive, royalty-free licence to reproduce, store and, with your specific consent, publish your content on our website.

You warrant and represent that your content will comply with these terms and conditions. Your content must not be illegal or unlawful, must not infringe any person's legal rights, and must not be capable of giving rise to legal action against any person (in each case in any jurisdiction and under any applicable law).

Your content, and the use of your content by us in accordance with these terms and conditions, must not:

infringe any copyright, trade mark or other intellectual property right;

be in breach of any contractual obligation owed to any person;

be untrue, false, inaccurate or misleading;

Privacy

Information collection and use - For a better experience while using our website, we may require you to provide us with certain personally identifiable information, including but not limited to your name, phone number and email address. The information that we collect may be used to contact or identify you.

If you use our website, you agree to the collection and use of information in relation with these terms and conditions. The personal information collected by us is used for providing and improving our services. We will not use or share your information with anyone except as described here.

Log data - Whenever you visit our website, we collect information that your browser sends to us including your computer’s Internet Protocol address, pages of our website visited by you, the time and date of your visit, the time spent on those pages, and other statistics.

Cookies – these are files with small amount of data that is commonly used as anonymous unique identifier. These are sent to your browser from the website and are stored on your computer’s hard drive. Our website uses these “cookies” to collection information and to improve our website. You have the option to either accept or refuse these cookies and know when a cookie is being sent to your computer. If you choose to refuse our cookies, you may not be able to use some portions of our Service.

Service providers - We may employ third-party companies and individuals to improve or repair our website and to assist with running our business activities etc. These third parties may have access to your personal information to perform the tasks assigned by us to them. However, they are obligated not to disclose or use the information for any other purpose.

We may suspend or cancel your account at any time in our sole discretion without notice or explanation.

Security - We value your personal information and strive to protect it and keep it confidential. But as no technology or system can be 100% secure and reliable, we cannot guarantee absolute security of your personal information.

Links to other sites - Our website may contain links to other sites. These external sites are not operated by us and we have no control over, and assume no responsibility for their content, privacy policies, or any other business practices.

Children’s privacy - Our website does not serve anyone under the age of 18. We do not knowingly collect personal identifiable information from children under 18. If you are a parent or guardian and you are aware that your child has provided us with personal information, please contact us so that we can delete their information and take any other necessary actions.

Breach of these terms and conditions

Without prejudice to our other rights under these terms and conditions, if you breach these terms and conditions in any way, or if we reasonably suspect that you have breached these terms and conditions in any way, we may suspend your access to our website, prohibit you permanently from accessing our website and/or commence suitable legal action against you, whether for breach of contract or otherwise.

Where we suspend or prohibit or block your access to our website or a part of our website, you must not take any action to circumvent such suspension or prohibition or blocking (including without limitation [creating and/or using a different account).

Amendments

We may revise these terms and conditions from time to time.

The revised terms and conditions shall apply to the use of our website from the date of publication of the revised terms and conditions on the website, and you hereby waive any right you may otherwise have to be notified of, or to consent to, revisions of these terms and conditions.

Privacy

You hereby agree that we may assign, transfer, sub-contract or otherwise deal with our rights and/or obligations under these terms and conditions.

You may not without our prior written consent assign, transfer, sub-contract or otherwise deal with any of your rights and/or obligations under these terms and conditions.

If a provision of these terms and conditions is determined by any court or other competent authority to be unlawful and/or unenforceable, other provisions will continue in effect.

The exercise of your and our rights under these terms and conditions is not subject to the consent of any third party.

The terms and conditions constitute the entire agreement between you and us in relation to your use of our website and supersede all such previous agreements between you and us.

These terms and conditions shall be governed by and construed in accordance with Indian Law.

Any disputes relating to these terms and conditions shall be subject to the exclusive jurisdiction of the courts of India.