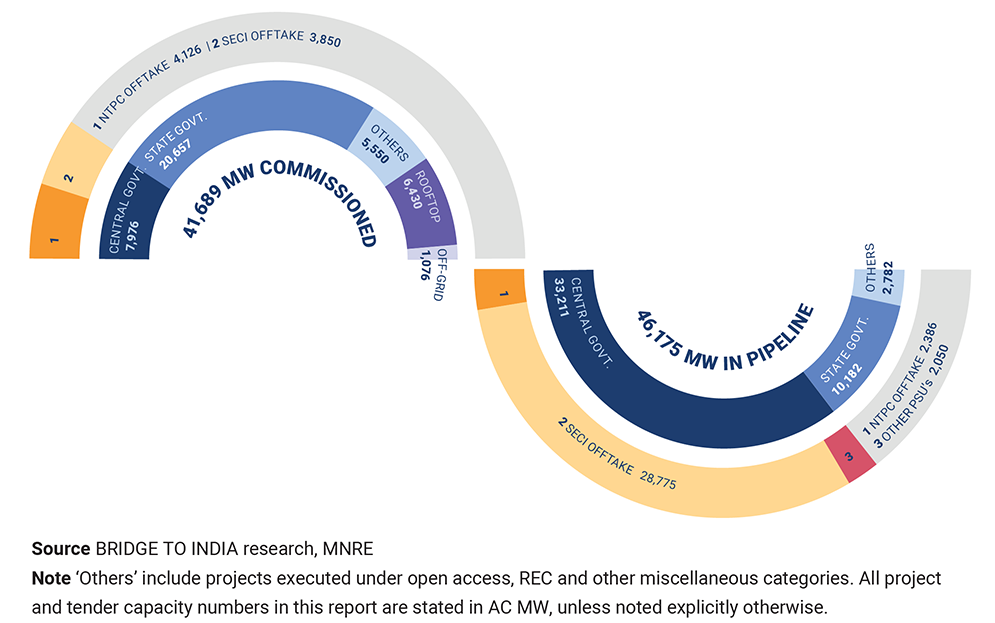

Coronavirus-induced hardships persisted in Q4 2020, pulling installation numbers down. Solar capacity addition in 2020 was at a five-year low. 1,298 MW of new capacity was added in the quarter, marginally below our estimate. Total installed capacity and project pipeline touched 41,689 MW and 46,175 MW, respectively by 31 December 2020.

Figure: Total installed and pipeline capacity by 31 December 2020, MW

Increase in module prices, other project costs coupled with COVID-induced operational and financial challenges continue to stall project construction activity. We expect construction pace to pick up in 2021 with record capacity addition of 16,000 MW in the year.

Reluctance of DISCOMs to sign PPAs is a concern with as much as 19,000 MW of auctioned projects yet to be tied-up. However, tender issuance and project auctions in Q4 were relatively robust at 32,014 MW and 28,050 MW, respectively. The quarter was notable for record low tariffs of INR 1.99-2.01/ kWh in the GUVNL 500 MW and SECI Rajasthan 1,070 MW auctions. Tariffs have dipped by 54% over last five years and by 18% over the last year. The low tariffs distort future tariff expectations of DISCOMs and raise risk of project cancellation or contract renegotiations.

This report provides a detailed update of all sector trends and developments in the quarter – ranging from capacity addition, leading players, tender and policy announcements, equipment prices, policy announcements, financial deals and other market developments. The report also provides market outlook for the next two quarters.

The report can be purchased online or by writing to us at market.research@bridgetoindia.com.