Gujarat recently announced a ban on private power consumers sourcing electricity from outside the state (refer). This is detrimental to India’s power sector reforms and hinders with the deployment of large-scale solar energy plants. The government should reconsider the decision, if it wants Gujarat to be a solar energy leader.

- India’s solar market is currently undergoing a transition from being policy-driven to being parity-driven. Rapid scale under a parity-driven market can only happen under a robust open access regulatory framework.

- Open access can work only if the country’s power sector reforms are pushed through. Given that national elections are underway in India, these reforms are unlikely to happen very soon.

- Large-scale power plants are critical to reducing the cost of solar, increasing efficiency and helping India meet its energy requirements. All large-scale power plants outside policy allocations must use the open access route to reach consumers.

The implications of this policy change are significant, especially for the solar sector. Gujarat leads the country in terms of total installed solar capacity with over 1 GW of installations. All this capacity has come as a part of state or national policies that promote solar power. In India, the solar market is now transitioning from policy-driven to parity-driven as several consumer segments reach grid parity with solar. For this very promising new market to develop successfully, smooth open access rules and practices are key.

Although open access is guaranteed to all consumers above 1 MW, utilities restrict this by refusing to grant applications. Often, grid congestions are cited as the reason. Although there is some merit to this, the concern is often not based on actual load flow studies. In many cases, the grid could well take solar power. Utilities also lobby at the state electricity regulatory commissions (SERCs) to increase open access changes – especially the Cross Subsidy Surcharge (CSS). India’s power tariffs are structured in such a manner that industrial and commercial consumers subsidize residential and agricultural consumers. When industries and commercial clients sign private power purchase agreements (PPAs), the utility loses out on these high value consumers. This is why a CSS is levied on consumers that shift to open access. While the interests of utilities have to be kept in mind, levying CSS and other charges does not help anybody. It keeps the utilities inefficient and hinders rapid deployment of renewable energies by keeping out private players from the power sector.

The real solution is to bring in an even power pricing mechanism and eliminate all subsidies. If power has to be subsidized for certain disadvantaged sections of the society then the subsidy amount must be borne by the state governments rather than passed on to the utilities. The Universal Identification Number (also called the Aadhar Card) could perhaps be used to target power subsidies to the poorest. Such a change in the power pricing structure requires strong political leadership. Gujarat has demonstrated such leadership in the past. Gujarat did two things rather successfully:

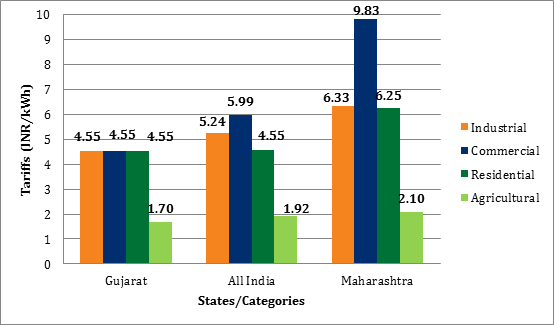

1) It freed up the State Electricity Regulatory Commission (SERC) from political interference and allowed periodic increases in tariffs. It also brought in a uniform power pricing and reduced cross subsidies significantly (see graph).

2) Gujarat separated unreliable agricultural feeders from domestic feeders for farmer’s homes. This meant that subsidized electricity was being used only to power water pumps and not farmer’s homes. Although this meant power prices went up for farmers, they now had reliable uninterrupted power. Farmers unanimously opted for paid power. The state government now subsidizes only the agricultural feeder (see graph). This resulted in a saving of INR 23,000 crore (INR 230 bn.) for the government[1].

Graph: Comparison of Gujarat’s power pricing across consumers with other states and India’s average.

Despite these tough measures that were considered political time bombs, Mr. Modi was voted back to power three times in a row. This goes to show that change is possible without jeopardizing political interests.

It therefore, comes as a particular surprise that Gujarat, which has so far led the transition towards a modern, competitive electricity economy, has decided to ban open access. This not only goes against Mr. Modi’s image as a pro market politician, but also jeopardizes his state’s electricity and solar success. Worryingly, this might just be a precedent for other states under pressure from entrenched utility interests to also ban open access.

[1] Business Today. http://businesstoday.intoday.in/story/gujarats-power-sector-turnaround-story/1/21750.html. February 5th 2012.

Akhilesh Magal is Senior Manager, Consulting at BRIDGE TO INDIA.